By Byron Gangnes

The unexpected election of Donald Trump has thrown a monkey wrench into forecasting the US and global economy. During the Presidential race, candidate Trump promised an array of dramatic policy changes, many of which could have dramatic economic impacts. The question now is which policies President Trump will in fact advance, which will be watered down or fall by the wayside, and whether Congress might have very different ideas.

President-elect Trump’s most controversial proposals could have profoundly negative economic effects. The biggest near-term concern is trade, where the President has broad latitude to act. He has threatened to impose large punitive tariffs on China and to “renegotiate” or abandon the North American Free Trade Agreement. Not only would unilateral US trade action be met with swift retaliation by trade partners, but it would be directly damaging to American firms, who now rely heavily on border-spanning global value chain production arrangements. Such actions would not return to the US lost manufacturing jobs, which have declined largely because of technological change. Instead, trade disruption would create losses across a broad swath of the American economy. In the near term, uncertainty about trade disruption could also damage investment in export-oriented sectors.

The proposed plans for massive tax cuts and infrastructure spending are more of a mixed bag. Attention to the nation’s decaying infrastructure is long overdue, but the timing of these actions is problematic. With the economy now close to full employment levels of activity, a dramatic fiscal stimulus could spark an acceleration of inflation. In response, the Fed would hike short-term interest rates, raising the risk of tipping the economy into recession. Trump’s policies as proposed would blow up the federal budget, leading to a higher government debt burden. Financial markets have moved in anticipation of at least some fiscal expansion, with equity markets rising on expected stronger demand and the likelihood of favored treatment for some industries, while bond markets have swooned under the fear of higher rates and higher inflation. It is unclear how far Congress will go in supporting the Trump fiscal agenda. It seems likely that only a more modest package of tax cuts and spending will get through, although the track record of fiscal restraint by past Republican Congresses is not good.

There are a number of areas where President-elect Trump’s proposals could have longer-term economic impacts, mostly on the negative side. The Trump agenda on immigration would be expensive and potentially very disruptive to labor markets and business operations. An overhaul of health care that did not adequately provide for the twenty million people who have obtained insurance under the Affordable Care Act would lead inevitably to a less healthy and less-productive labor force. Tax cuts that primarily benefit wealthier households would exacerbate existing problems of income inequality, class resentment, and political polarization. A poorer trade environment would hamper US and global growth. Stacked up against these fairly tangible risks is the less certain possibility that lower taxes and a reasoned approach to regulatory reform might spur efficiency gains.

At this point, there is simply a lot we do not know. It seems likely that many of the most extreme actions that President-elect Trump raised on the campaign trail will be moderated in their implementation. In some cases he has already telegraphed his intent to do so. At the same time, his mercurial nature makes it very difficult to know how he will proceed once in office.

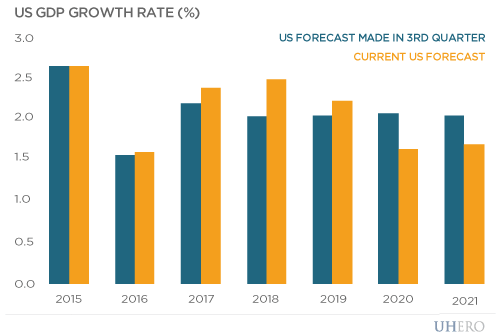

For a forecaster, the question is how to build in assumptions about future policy when so much remains uncertain. For now, we have adjusted upward modestly our forecast for gross domestic product in 2017 to 2019, to reflect moderate fiscal stimulus. We have adjusted downward by a bit our forecast for subsequent years, reflecting our view that the changing environment for trade, immigration, and income inequality will have a persistent depressing effect on growth over the medium term. Expect us to make further adjustments to our US and global economic outlook as the policy picture becomes clearer in 2017.

BLOG POSTS ARE PRELIMINARY MATERIALS CIRCULATED TO STIMULATE DISCUSSION AND CRITICAL COMMENT. THE VIEWS EXPRESSED ARE THOSE OF THE INDIVIDUAL AUTHORS. WHILE BLOG POSTS BENEFIT FROM ACTIVE UHERO DISCUSSION, THEY HAVE NOT UNDERGONE FORMAL ACADEMIC PEER REVIEW.